May 7, 2024

Luis Alvarado, Global Fixed Income Strategist

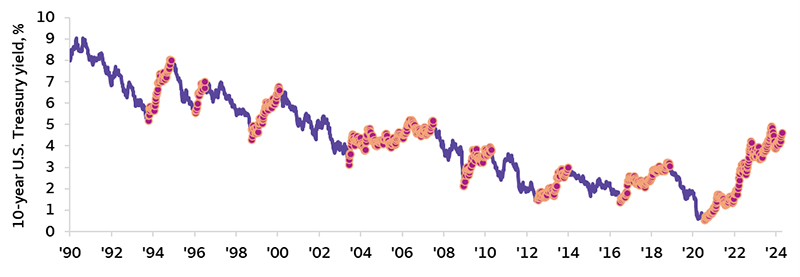

Implications of Fed policy for Treasury yields

Sources: Wells Fargo Investment Institute and Bloomberg, as of April 19, 2024. Weekly data from January 2, 1990, to April 19, 2024. Rising yield periods highlighted in orange and pink dotted areas. Past performance is no guarantee of future results. Excerpted from Investment Strategy (April 29)

Sources: Wells Fargo Investment Institute and Bloomberg, as of April 19, 2024. Weekly data from January 2, 1990, to April 19, 2024. Rising yield periods highlighted in orange and pink dotted areas. Past performance is no guarantee of future results. Excerpted from Investment Strategy (April 29)Our higher-for-longer bias supported by higher real rates and inflation expectations

The Federal Open Market Committee (FOMC) kept the federal funds rate unchanged at 5.25% – 5.50% for the sixth straight meeting as of May 1. As expected, the Federal Reserve (Fed) pointed out that the trajectory of inflation remains worrisome, and it is still not prepared to cut rates. This may leave investors wondering how Treasuries are likely to perform amid the now-solidified narrative of higher-for-longer rates.

The chart above provides a long-term perspective of 10-year Treasury yields, filled with periods of rising and declining yields. For now, we do not envision yields entering a declining trend. Quite the opposite, the current trend is for long-term yields to remain higher, supported by positive real rates above 2.2% and stickier inflation expectations around 2.3% (10-year breakeven inflation expectations). Considered in conjunction, these numbers suggest that 10-year Treasury yields will likely remain near their recent range, in line with our year-end 2024 target range of 4.25% – 4.75%.

What it may mean for investors

Our current view is that the Fed will attempt to cut rates twice before year end; however, the probability for the federal funds rate to remain on hold at current levels is increasing as inflation remains sticky. Accordingly, we continue to position portfolios defensively. We believe fixed-income investors may benefit by being most favorable short-term fixed income and neutral intermediate and long term. We expect the yield curve to continue to flatten, but events that could push 10-year U.S. Treasury yields toward 5% include the Fed openly removing rate cut expectations or outright hiking; inflation climbing higher; real gross domestic product growth increasing; or the U.S. fiscal situation deteriorating.

Risk Considerations

Forecasts, estimates, and projections are not guaranteed and are based on certain assumptions and views of market and economic conditions which are subject to change.

Investments in fixed-income securities are subject to interest rate, credit/default, liquidity, inflation and other risks. Bond prices fluctuate inversely to changes in interest rates. Therefore, a general rise in interest rates can result in the decline in the bond’s price. Credit risk is the risk that an issuer will default on payments of interest and principal. This risk is higher when investing in high yield bonds, also known as junk bonds, which have lower ratings and are subject to greater volatility. If sold prior to maturity, fixed income securities are subject to market risk. All fixed income investments may be worth less than their original cost upon redemption or maturity.

Although Treasuries are considered free from credit risk they are subject to other types of risks. These risks include interest rate risk, which may cause the underlying value of the bond to fluctuate.

General Disclosures

Global Investment Strategy (GIS) is a division of Wells Fargo Investment Institute, Inc. (WFII). WFII is a registered investment adviser and wholly owned subsidiary of Wells Fargo Bank, N.A., a bank affiliate of Wells Fargo & Company.

The information in this report was prepared by Global Investment Strategy. Opinions represent GIS’ opinion as of the date of this report and are for general information purposes only and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally. GIS does not undertake to advise you of any change in its opinions or the information contained in this report. Wells Fargo & Company affiliates may issue reports or have opinions that are inconsistent with, and reach different conclusions from, this report.

The information contained herein constitutes general information and is not directed to, designed for, or individually tailored to, any particular investor or potential investor. This report is not intended to be a client-specific suitability or best interest analysis or recommendation, an offer to participate in any investment, or a recommendation to buy, hold or sell securities. Do not use this report as the sole basis for investment decisions. Do not select an asset class or investment product based on performance alone. Consider all relevant information, including your existing portfolio, investment objectives, risk tolerance, liquidity needs and investment time horizon. The material contained herein has been prepared from sources and data we believe to be reliable but we make no guarantee to its accuracy or completeness.

Wells Fargo Advisors is registered with the U.S. Securities and Exchange Commission and the Financial Industry Regulatory Authority, but is not licensed or registered with any financial services regulatory authority outside of the U.S. Non-U.S. residents who maintain U.S.-based financial services account(s) with Wells Fargo Advisors may not be afforded certain protections conferred by legislation and regulations in their country of residence in respect of any investments, investment transactions or communications made with Wells Fargo Advisors.

Wells Fargo Advisors is a trade name used by Wells Fargo Clearing Services, LLC and Wells Fargo Advisors Financial Network, LLC, Members SIPC, separate registered broker-dealers and non-bank affiliates of Wells Fargo & Company.